Quick Answer

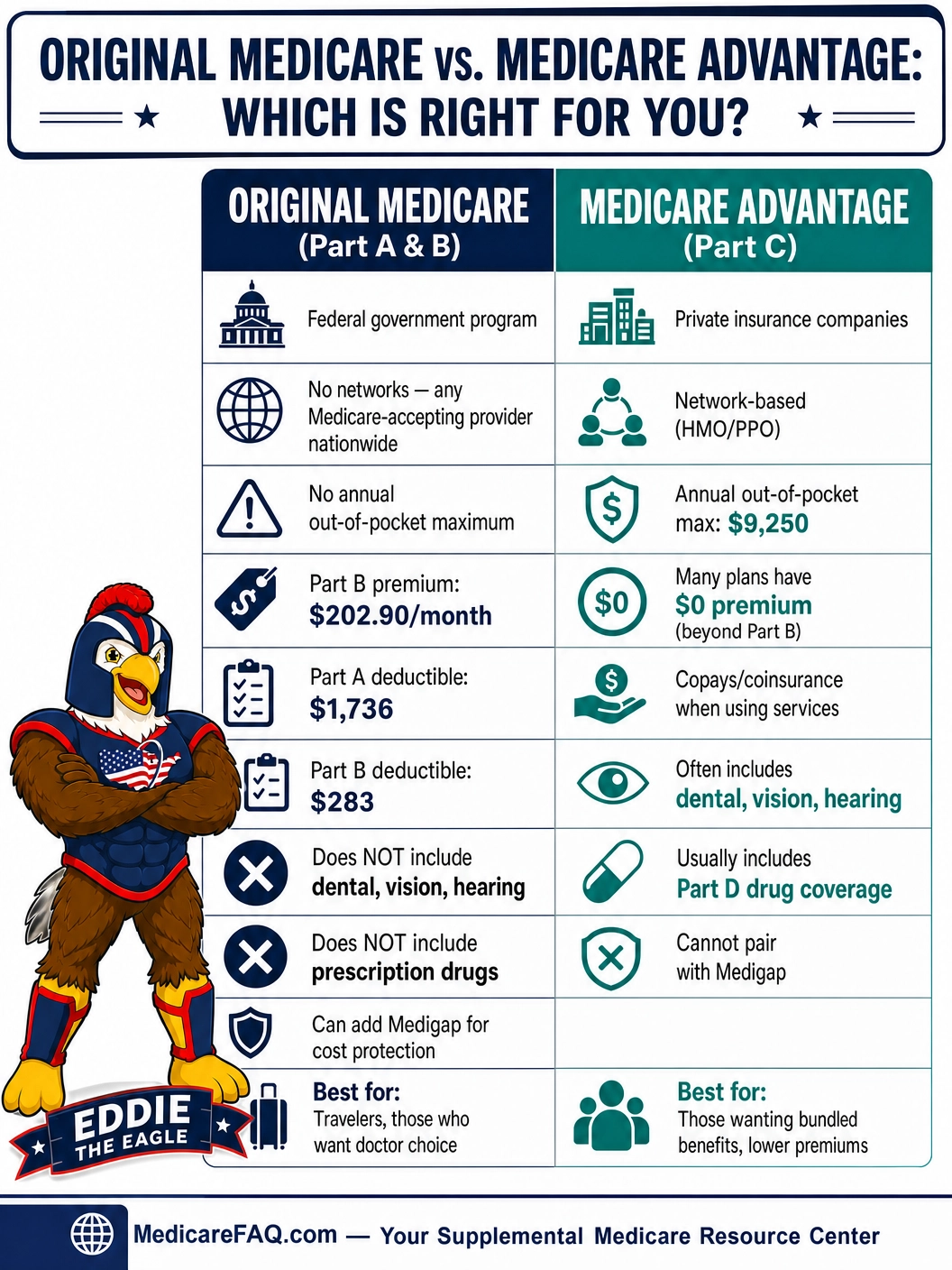

Original Medicare (Part A & B) offers nationwide provider access with no networks but has no out-of-pocket maximum. Medicare Advantage (Part C) bundles coverage through private insurers with added benefits but restricts you to provider networks.

Coverage Comparison by Plan Type

| Plan Type | Coverage | Notes |

|---|---|---|

| Original Medicare (Part A & B) | Federal Program | Government-administered; any Medicare-accepting provider nationwide |

| Medicare Advantage (Part C) | Private Plans | Private insurers; network-based with added benefits like dental/vision |

| Medigap (Supplement) | Pairs with Original | Fills Original Medicare cost-sharing gaps; cannot pair with MA |

| Medicare Part D | Separate or Bundled | Standalone with Original Medicare; often bundled in MA plans |

Understanding Your Coverage Options

Original Medicare (Part A & Part B)

Government-AdministeredOriginal Medicare is the federal health insurance program administered directly by the government. It consists of Part A (hospital insurance) and Part B (medical insurance). You earn Part A eligibility by paying Medicare taxes throughout your working career - typically requiring 40 quarters (10 years) of work.

Every beneficiary enrolled in Original Medicare receives identical benefits regardless of where they live. There are no provider networks, no copays for most services, no waiting periods, and no pre-existing condition limitations. You can see any doctor or specialist that accepts Medicare assignment anywhere in the United States without a referral.

Your coverage travels with you across all 50 states. If you live in California and need care while visiting Florida, your benefits remain exactly the same. This nationwide portability is one of Original Medicare's strongest advantages for retirees who travel frequently.

However, Original Medicare has no annual out-of-pocket maximum, which means your cost-sharing (deductibles, coinsurance) is unlimited. In 2026, the Part B premium is $202.90/month, the Part A deductible is $1,736 per benefit period, and the Part B deductible is $283/year. After meeting deductibles, you typically pay 20% coinsurance for Part B services with no cap. Original Medicare also does not cover routine dental, vision, hearing, or prescription drugs - you need separate policies for those.

What It Covers

- Hospital stays (Part A) - semi-private room, meals, nursing care

- Outpatient medical services (Part B) - doctor visits, lab tests, preventive care

- Skilled nursing facility care (up to 100 days per benefit period)

- Home health services and hospice care

- Durable medical equipment (wheelchairs, walkers, oxygen)

- Preventive services - annual wellness visits, screenings, vaccines

What It Doesn't Cover

- Routine dental, vision, and hearing care

- Prescription drugs (need separate Part D plan)

- Long-term custodial care

- Care outside the United States (with limited exceptions)

- Cosmetic surgery

2026 costs: Part B premium $202.90/month, Part A deductible $1,736/benefit period, Part B deductible $283/year, then 20% coinsurance with no annual cap.

Pair with Medigap for Cost Protection

Because Original Medicare has no out-of-pocket maximum, many beneficiaries pair it with a Medicare Supplement (Medigap) plan to cover deductibles and coinsurance. Plans like Medigap Plan G can reduce your annual out-of-pocket exposure to just the $283 Part B deductible.

Medicare Advantage (Part C)

Private InsuranceMedicare Advantage plans are offered by private insurance companies approved by Medicare. These plans must cover everything Original Medicare covers, but they can structure cost-sharing differently and add extra benefits. Medicare pays the private insurer a fixed amount per enrollee, and the insurer manages your healthcare benefits under Medicare Part C.

Most Medicare Advantage plans operate as HMOs (Health Maintenance Organizations) or PPOs (Preferred Provider Organizations), meaning you must use in-network providers or pay significantly more for out-of-network care. Many HMO plans require you to choose a primary care physician who coordinates your care and provides referrals to see specialists.

A key advantage of Medicare Advantage is the annual out-of-pocket maximum - capped at $9,250 for in-network services in 2026. Once you hit this limit, the plan pays 100% of covered services for the rest of the year. Many plans also bundle prescription drug coverage (Part D), dental, vision, hearing, and fitness benefits at no additional premium beyond your Part B premium.

However, Medicare Advantage plans change annually. Networks shrink, benefits get modified, and the plan that works for you this year may not work next year. Physicians can leave a plan's network at any time, potentially disrupting your care. Additionally, coverage typically does not travel well - if you spend significant time outside your plan's service area, you may have limited or no coverage except for emergencies.

What It Covers

- Everything Original Medicare covers (Part A & B services)

- Annual out-of-pocket maximum ($9,250 in-network in 2026)

- Often includes Part D prescription drug coverage

- Many plans add dental, vision, and hearing benefits

- Some plans offer fitness programs (SilverSneakers, gym memberships)

- Some plans offer Part B premium give-back benefits

What It Doesn't Cover

- Out-of-network care (HMO plans - except emergencies)

- Services outside the plan's service area (non-emergency)

- Benefits may change annually - not guaranteed year to year

- Cannot pair with a Medigap plan

Many plans have $0 premiums beyond your Part B premium ($202.90/month in 2026), but cost-sharing (copays, coinsurance) applies when you use services.

Network Restrictions Matter

Unlike Original Medicare, Medicare Advantage plans restrict which doctors and hospitals you can use. If your preferred provider leaves the network mid-year, you may need to find a new doctor or wait until the next enrollment period to switch plans.

Medicare Supplement (Medigap)

Medicare Supplement (Medigap) plans are sold by private insurers but work very differently from Medicare Advantage. Instead of replacing Original Medicare, Medigap plans supplement it - they pay the cost-sharing gaps (deductibles, coinsurance, copayments) that Original Medicare leaves behind.

You cannot have both a Medicare Advantage plan and a Medigap plan at the same time. Medigap only works with Original Medicare. If you choose the Original Medicare + Medigap route, you keep all the benefits of Original Medicare (nationwide access, no networks, no referrals) while gaining financial protection against high out-of-pocket costs.

The most popular Medigap plan in 2026 is Plan G, which covers everything except the annual Part B deductible ($283). This means your total annual out-of-pocket exposure with Plan G is just $283 plus your monthly premiums - far more predictable than either Original Medicare alone or Medicare Advantage.

Medigap vs. Medicare Advantage - You Must Choose

You cannot hold both a Medigap plan and a Medicare Advantage plan simultaneously. If you want Medigap, you must be enrolled in Original Medicare (Part A & B). If you switch to Medicare Advantage, your Medigap plan must be dropped.

✦ Frequently Asked Questions

David Haass

AuthorDavid Haass is the Chief Technology Officer and Co-Founder of Elite Insurance Partners and MedicareFAQ.com. He is a member and regular contributor to Forbes Finance Council.

Ashlee Zareczny

ReviewerAshlee Zareczny is a licensed Medicare agent dedicated to helping those eligible for Medicare find the best coverage options.